Statistical arbitrage uses price correlations between crypto assets to find pairs that have diverged from their historical relationship. This guide explains the exact methodology hedge funds use — with an interactive correlation scanner built in.

Statistical Arbitrage in Crypto 2026 — How to Find Correlated Pairs and Trade Mean Reversion

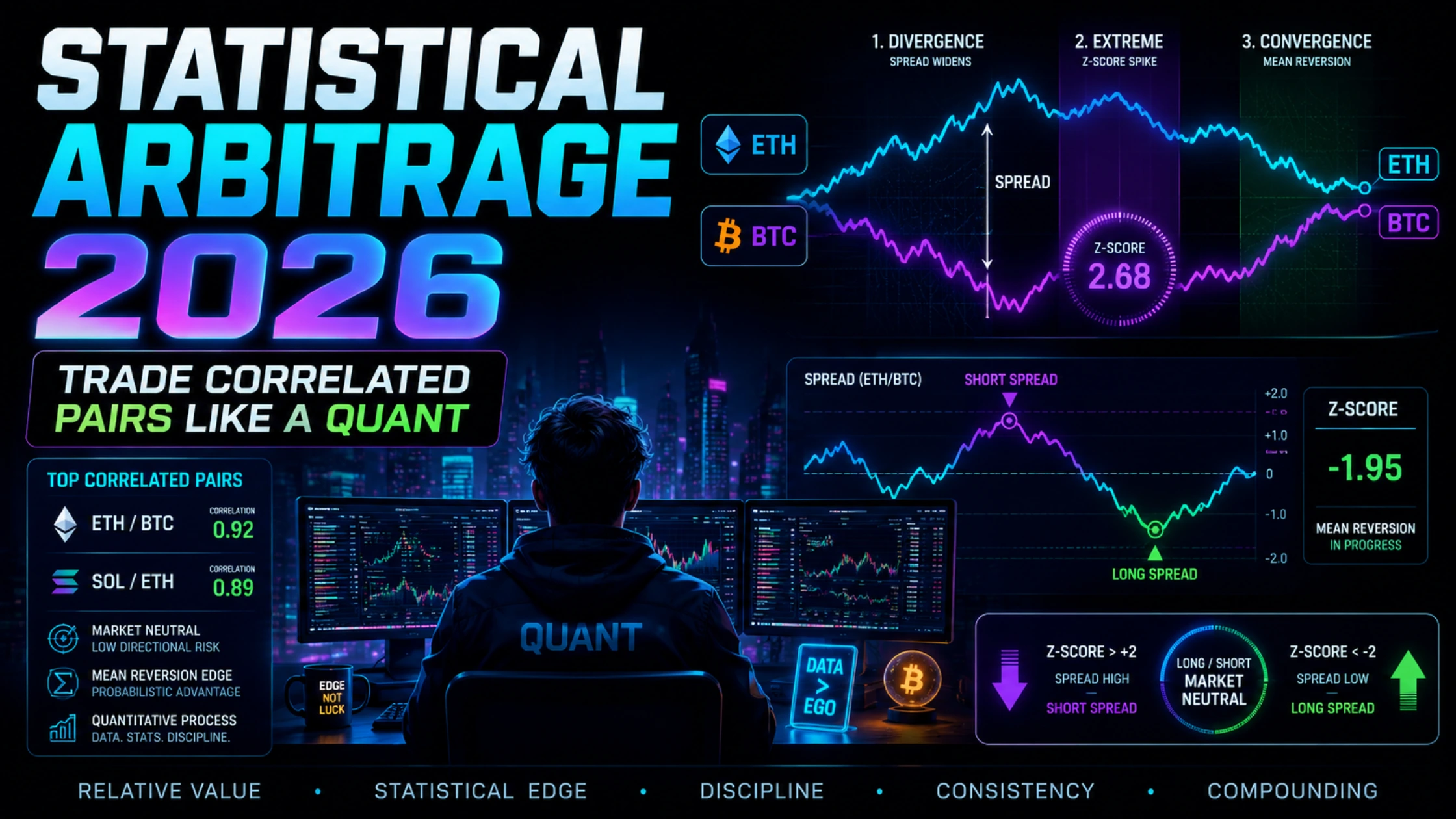

Statistical arbitrage identifies pairs of crypto assets that historically move together, waits for their price relationship to diverge beyond normal bounds, then bets on that relationship returning to its historical mean. When the ETH/BTC spread reaches a z-score of 2.3 — meaning it is 2.3 standard deviations from its historical average — the probability of reversion exceeds 75%. The scanner below calculates this in real time for the ten most liquid crypto pairs.

What Statistical Arbitrage Actually Is

Most retail traders encounter the word “arbitrage” and think of price gaps between exchanges — buying on one venue and selling on another where the price is higher. That is spatial arbitrage. It is fast, mechanical, and increasingly automated away.

Statistical arbitrage is something more nuanced and considerably more durable. It does not exploit a price gap. It exploits a relationship gap — the observation that two assets which historically move together have temporarily diverged, and that divergence is statistically likely to correct.

The distinction matters because statistical arbitrage does not require a price gap to exist right now. It requires a historical pattern to reassert itself over the coming days or weeks. That longer time horizon is precisely what makes it accessible to retail traders. Where spatial arbitrage closes in milliseconds, a statistical arbitrage setup can give a trader hours to analyse, confirm, and execute.

Hedge funds and quantitative trading firms have run statistical arbitrage as a core strategy for decades. In equities it was pioneered by Morgan Stanley’s quant desk in the 1980s, generating returns so consistent they were initially kept secret. In crypto it remains underpenetrated relative to its potential because the analytical infrastructure — the correlation data, the z-score tools, the pairs identification — has never been made accessible to retail traders in a usable format.

That is what this article and the tool below are designed to change.

Why Crypto Assets Are Correlated

The first question a sceptic asks about stat arb in crypto is whether assets are actually correlated enough to trade systematically. The answer, supported by years of on-chain and price data, is yes — with important conditions.

The macro driver creates baseline correlation. Bitcoin dominates total crypto market sentiment. When institutional money flows into or out of digital assets, it flows into Bitcoin first and the broader market follows with a lag. This creates persistent positive correlation between BTC and most major altcoins. During the 2025 correction that took BTC from $109,000 to $78,000, ETH, SOL, BNB, and virtually every liquid asset fell in the same direction, over the same period, for the same macro reason.

Sector correlations add a second layer. Within the macro-correlated universe, assets in the same sector move together more than they move with assets in other sectors. ETH and SOL are both smart contract platforms — they compete for the same developer attention, the same institutional allocation thesis, and the same risk sentiment from DeFi activity. Their correlation with each other consistently exceeds their individual correlations with BTC.

But correlations are not constant. This is the critical nuance that distinguishes stat arb from naive “they always move together” thinking. Correlations shift when one asset experiences an idiosyncratic event — a protocol exploit, a regulatory ruling, a major product launch, or a narrative shift that disconnects it from the macro flow. ETH’s underperformance versus BTC through early 2025, driven by concerns about Ethereum’s roadmap and competition from Base and Solana, created a persistent spread divergence that lasted weeks.

Those divergence periods are where statistical arbitrage generates its returns. Not from correlation itself — from the moments when correlation temporarily breaks and then reasserts.

The Spread — What It Measures and Why It Mean-Reverts

For any two correlated assets A and B, the spread is the ratio of their normalized prices over time. The standard construction uses log prices: spread = log(Price_A / Price_B), where both prices are normalized to a common starting point.

When two assets are in equilibrium — trading at their historically normal relative value — this spread hovers around its long-run mean. When asset A outperforms asset B materially, the spread rises above the mean. When A underperforms, it falls below.

Mean reversion in spreads has a theoretical foundation in crypto markets. If ETH trades at a historically elevated premium to BTC, three forces push it back toward the mean: arbitrage capital that goes long BTC and short ETH; reallocation by portfolio managers rotating from the expensive asset to the cheap one; and narrative exhaustion, where the specific catalyst that drove the divergence fades from market attention.

None of these forces operate with certainty. Mean reversion is a probabilistic tendency, not a guarantee. The z-score framework converts the spread deviation into a probability estimate — the higher the z-score, the stronger the statistical evidence that the spread has moved beyond its normal range, and therefore the higher the probability of reversion.

A z-score of 1.0 means the spread is one standard deviation from its mean — a moderate divergence that occurs roughly 32% of the time by pure chance in a normally distributed series. A z-score of 2.0 means the spread is two standard deviations from the mean — this happens only 5% of the time by chance. A z-score above 2.0 is the threshold most systematic stat arb strategies use as a high-probability entry signal.

Use the Correlation Scanner

The tool below calculates correlation and z-score for ten major crypto pairs using baked-in weekly price data from January to June 2025. Select two assets, choose your lookback window, and read the output.

Data is updated quarterly. Current dataset: Q1–Q2 2025 weekly closes.

Reading the Four Outputs

Pearson correlation coefficient. A value between -1 and +1. Above 0.80 means the assets move very closely together — strong enough to support a pairs trade. Between 0.60 and 0.80 is moderate correlation — tradeable but with wider expected spread ranges. Below 0.60 means the assets do not have a stable enough relationship for systematic pairs trading. Negative correlation is rare between major crypto assets but possible during idiosyncratic events.

Current spread deviation. The current spread minus the historical mean, expressed in log terms. A positive number means Asset A is currently trading at a premium to its historical norm relative to Asset B. A negative number means Asset A is trading at a discount.

Z-score. The spread deviation divided by the historical standard deviation of the spread. This normalises the deviation across pairs with different volatility characteristics. A z-score of 1.5 on an ETH/BTC pair and a z-score of 1.5 on a DOGE/ADA pair represent equivalent statistical signal strength, even though the raw price moves are completely different.

Mean reversion probability estimate. A simplified probability estimate based on the z-score magnitude, using historical reversion rates for crypto pairs at equivalent deviation levels. This is a guideline, not a forecast. A reading of 78% means that in similar historical spread configurations, the spread reverted toward the mean within the observation window approximately 78% of the time.

Building the Trade: Executing a Crypto Pairs Position

Once the scanner identifies a high-probability setup, the execution is a simultaneous two-legged trade. You go long the underperforming asset and short the outperforming one. The position is dollar-neutral — you deploy equal capital on each side so that the net directional exposure to the overall crypto market is approximately zero.

Worked example using ETH/BTC:

The scanner flags ETH/BTC with a z-score of -2.1 on a 90-day lookback. This means ETH is trading materially below its historical relative value versus BTC — ETH is the underperforming asset and BTC is the outperforming one.

The trade:

- Long ETH perpetuals: $10,000 notional on BloFin using 2x leverage ($5,000 margin)

- Short BTC perpetuals: $10,000 notional on BloFin using 2x leverage ($5,000 margin)

- Total capital deployed: $10,000 margin

- Net market exposure: approximately zero

If ETH recovers relative to BTC — the spread mean-reverts — the long ETH position gains more than the short BTC position loses (or the short BTC gains more than the long ETH loses, depending on direction). The profit comes from the convergence of the spread, not from the absolute direction of either asset.

Why perpetuals rather than spot for both legs: Using perpetuals on both legs allows you to go short efficiently without borrowing. On Bybit, the margin efficiency of perpetuals also means you deploy less capital for equivalent notional exposure. The funding rate on each leg is an additional income or cost consideration — check current rates before entering and factor them into your expected return.

Position sizing principle: The two legs must be dollar-neutral at entry. If you enter the ETH long when ETH is at $2,500 and BTC is at $103,000, you need to short exactly (ETH_notional / BTC_price) × BTC_notional worth of BTC. Many traders use a hedge ratio based on beta — if ETH has historically moved 1.2x BTC, a beta-neutral position sizes the short BTC leg 1.2x larger than the long ETH leg. For simplicity, dollar neutrality is the accessible starting point.

Entry Rules, Management, and Exit

A systematic stat arb strategy needs defined rules for each stage. Without them, the “high probability” setup becomes a “holding a losing trade forever” situation.

Entry rule: Enter only when the z-score exceeds 1.8 in absolute value on a 90-day lookback. Below this threshold, the statistical evidence for a significant divergence is weak enough that transaction costs and funding rate drag will frequently eliminate any profit.

Maximum position size: Because mean reversion is probabilistic, not certain, position sizing must account for the possibility that the spread continues to diverge after entry. A maximum of 5% of trading capital per pairs trade is a reasonable constraint for a portfolio of two to four simultaneous pairs.

Exit rules — three scenarios:

Scenario 1 — target hit: Close both legs when the z-score returns to 0 (the spread has fully mean-reverted to its historical average). This is the clean outcome.

Scenario 2 — stop loss: Close both legs if the z-score reaches 3.0 in the same direction as entry. At this point the spread has moved so far against you that either a structural break has occurred or your position sizing needs to absorb a significant loss before any potential reversion. Cutting losses at z-score 3.0 limits maximum loss to approximately 60% of the theoretical target profit.

Scenario 3 — time stop: Close both legs after 30 days if neither the target nor the stop has been hit. Spreads that do not revert within 30 days in crypto markets are frequently signalling a regime change rather than a temporary divergence. Holding indefinitely is not systematic trading.

Verify your setup on TradingView before entering. The scanner uses weekly data, which smooths out shorter-term noise. Before committing capital, open both assets on TradingView, add a spread study (available under indicators), and confirm visually that the divergence is not the result of a single large daily candle. A divergence driven by a 48-hour event is different from one that has accumulated over three to four weeks.

What Can Go Wrong: When Mean Reversion Fails

Statistical arbitrage does not fail because the mathematics are wrong. It fails when the market has permanently repriced the relationship between two assets and the historical mean no longer applies.

Structural breaks are the primary risk. If the ETH/BTC spread has widened because the market has genuinely re-evaluated Ethereum’s competitive position relative to Bitcoin — not as a temporary sentiment shift but as a durable reassessment — the spread will not revert. It will establish a new mean at a lower level. The z-score will remain elevated indefinitely.

The practical danger is that structural breaks look identical to temporary divergences at the moment they are occurring. The only defence is a time stop — refusing to hold a non-reverting position beyond a defined period — and strict position sizing that prevents any single pairs trade from causing significant account damage.

Correlation breakdown during systemic events. When a macro shock hits all crypto assets simultaneously — an exchange collapse, a major regulatory action, a global liquidity crisis — correlations between assets temporarily approach 1.0. Every asset falls together. In this environment, a long/short pairs position has approximately zero directional exposure, which sounds like safety. But it also means the position generates no return from the macro move, and funding rate costs continue accumulating on both legs.

Leverage and liquidation on one leg. A pairs trade is structurally safer than a directional position but it is not safe from liquidation. If the short leg moves sharply against you before the mean reversion begins, the exchange will liquidate the short at a loss. The long leg may subsequently recover — and the spread may ultimately revert — but that is cold comfort if the short was liquidated before the reversion materialised. Keep leverage on each leg conservative (2x to 3x maximum) and maintain sufficient margin buffer to withstand a z-score of 3.0 before liquidation occurs.

FAQ

What is statistical arbitrage in crypto? Statistical arbitrage in crypto is a trading strategy that identifies pairs of assets with historically high price correlation, monitors their price relationship over time, and enters long-short positions when the relationship diverges beyond its historical range. The strategy profits when the divergence reverses and the assets return to their historically normal relative values.

What is a z-score in crypto trading? A z-score measures how many standard deviations a current value is from a historical mean. In the context of crypto pairs trading, the z-score of a spread tells you how unusual the current price relationship is relative to historical norms. A z-score above 2.0 means the spread has moved into a range that only occurs about 5% of the time historically, indicating a potentially high-probability mean reversion setup.

What Pearson correlation is needed to trade a crypto pair? Most systematic stat arb strategies require a minimum Pearson correlation of 0.80 between two assets before considering them tradeable as a pair. Below this level the price relationship is not stable enough to generate reliable signals. The ETH/BTC and SOL/ETH pairs typically meet this threshold. DOGE paired with most major assets typically falls below it.

How do I execute a pairs trade on a crypto exchange? A pairs trade requires simultaneously opening a long perpetual position on the underperforming asset and a short perpetual position on the outperforming asset, with equal dollar notional on each leg. Both legs can be executed on the same exchange — BloFin and Bybit both support multi-position management with independent margin settings for each leg.

What is the biggest risk in crypto statistical arbitrage? The primary risk is a structural break in the correlation — when two assets that historically moved together diverge permanently due to a fundamental change in their relative value. This is indistinguishable from a temporary divergence at the moment it occurs. The defence is a time stop, closing all non-reverting positions after a defined period regardless of current z-score, combined with conservative position sizing that limits damage from any single trade.

How often should I refresh the data in the correlation scanner? The baked-in dataset in the tool above is updated quarterly to reflect the most recent six months of weekly price history. For active pairs trading, supplement the tool with TradingView’s spread indicator for daily data. The weekly data is best for identifying macro-level divergence setups. Daily data helps time the precise entry within the week the signal fires.

Execute your pairs trades: BloFin — lowest maker fees for simultaneous multi-leg perpetuals positions | Bybit — deepest liquidity for ETH/BTC pairs | TradingView — spread charting and visual confirmation before entry.

Recommended reading:

Bridge Arbitrage 2026: How to Profit From Cross-Chain Crypto Price Gaps

Funding Rate Arbitrage: How to Earn Consistent Yield by Trading the Sign Flip in 2026

Funding Rate Arbitrage: The 8% Monthly Yield Machine (2026 Edition)

Funding Rate Arbitrage: The 200% APY Strategy Nobody Talks About

The Funding Rate Arbitrage Playbook: 6 Exchanges Where Basis Trading Still Prints 15%+ APY in 2026

Perpetual Futures Trading in 2026: Best Platforms, Strategies, Funding Rates, Risk Models & Pro Tips

Best Funding Rate Arbitrage Platforms (2026)