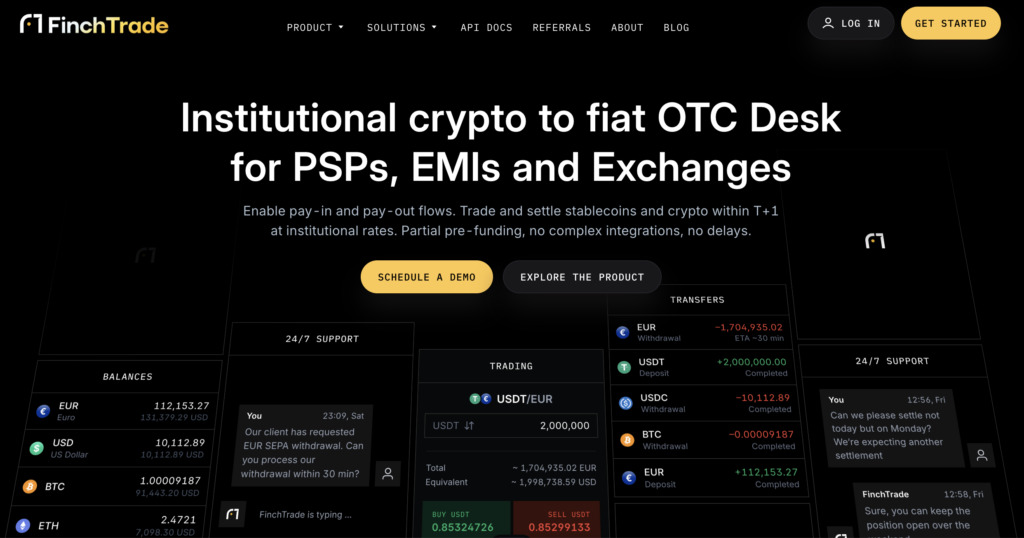

FinchTrade is a Swiss-licensed institutional OTC desk offering stablecoin settlement, crypto-fiat conversion, and cross-border payment infrastructure for PSPs, EMIs, and crypto exchanges, with ~30-minute settlement.

There is a category of infrastructure company that never makes headlines. It exists, quietly and profitably, in the pipes: the settlement rails, the liquidity bridges, the compliance corridors that institutions depend on to move large sums of money across borders without friction, delay, or catastrophic counterparty risk. No token. No retail product. No Coingecko listing.

FinchTrade, headquartered in Zug, Switzerland, and operating under a VASP licence through the Swiss VQF self-regulatory body, has built an institutional OTC desk for the entities that sit one layer above the end user: payment service providers, electronic money institutions, crypto exchanges, and OTC desks that need deep, reliable liquidity at sizes and speeds that consumer platforms simply cannot deliver.

What FinchTrade Actually Does

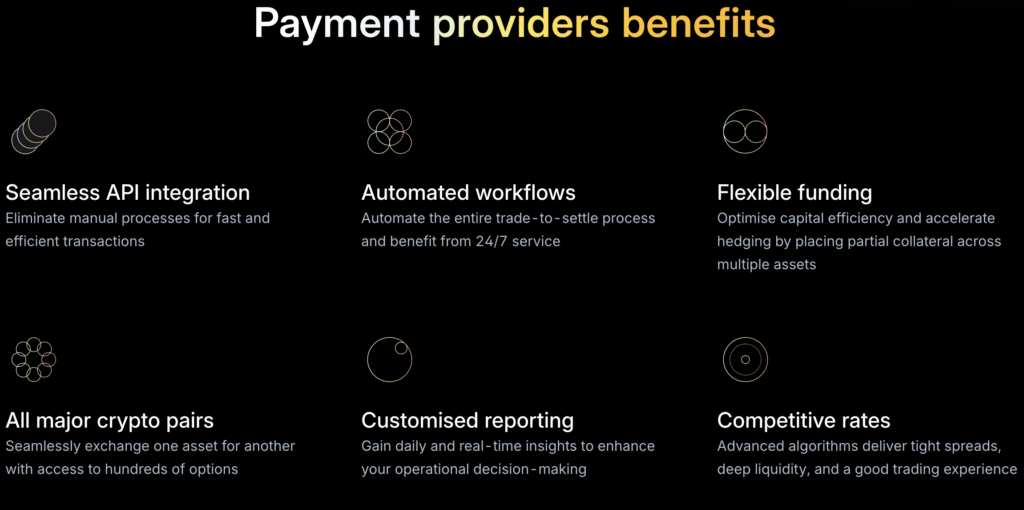

At its core, FinchTrade’s product handles three functions: large institutional crypto-to-fiat and fiat-to-crypto trades at tight spreads with execution up to €10 million per transaction; settlement of those trades in approximately 30 minutes, 24/7 including weekends; and connection to real banking rails including SEPA, SEPA Instant, SWIFT, BLINC, ACH, Fedwire, FPS, and CHAPS, through banking partners including BCB Group, ClearJunction, Nexpay, FV Bank, and Fiat Republic.

Supported assets include USDT, USDC, and EURC across Ethereum, Polygon, Solana, and Tron, plus Bitcoin, Ethereum, XRP, ADA, LTC, and DOGE. Fiat settlement covers EUR, USD, GBP, CHF, and AED. According to the Finery Markets State of Crypto OTC report, stablecoins reached a market cap of approximately $310 billion with $57 trillion in annual transaction volume as of January 2026. That volume is not driven by retail speculation. It is driven by PSPs converting merchant receipts, EMIs managing cross-border float, and businesses using USDT and USDC as working capital rails in markets where fiat banking is slow, expensive, or unreliable. That is the environment FinchTrade was built for, and where its $1 billion in client trading volume since 2025 has been accumulated.

The infrastructure stack includes Fireblocks for custody and Scorechain and Sumsub for AML/KYT monitoring and KYB onboarding. These are not names that appear on consumer-facing products; they are the building blocks of institutional-grade plumbing, and their presence signals who FinchTrade is genuinely built for.

The Pre-Funding Problem No One Talks About

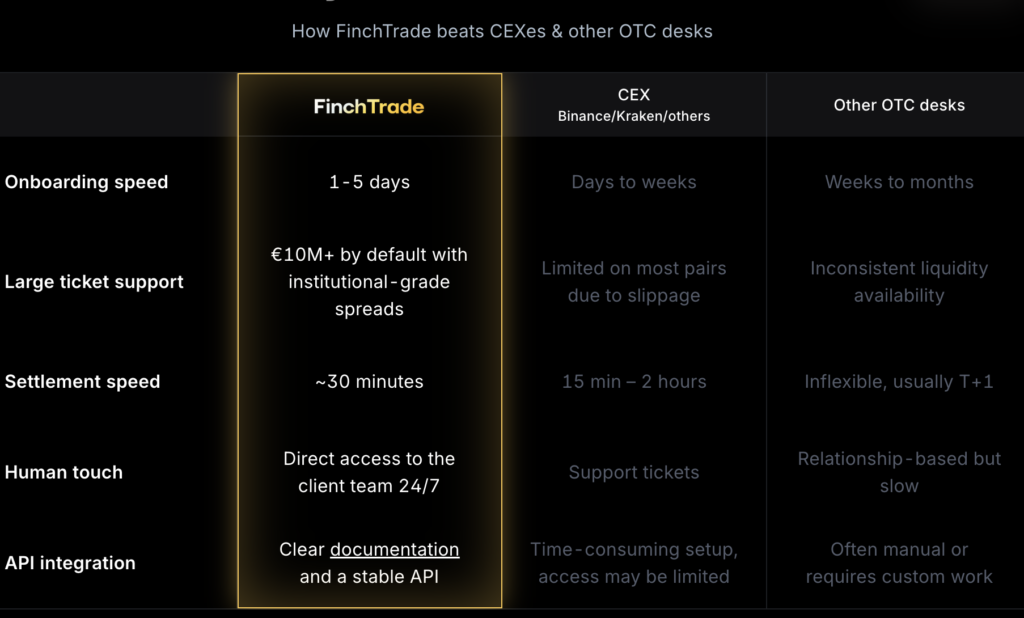

One of the most underappreciated structural inefficiencies in institutional crypto is pre-funding. Most OTC desks and centralised exchanges require clients to deposit the full notional amount, or more, before any execution takes place.

For a PSP or EMI running meaningful volume, the cost is real. A company processing €5 million in crypto payments per week needs that capital sitting idle across multiple accounts, locked and unproductive, purely to satisfy a counterparty’s operational requirements. Capital that could be deployed elsewhere earns nothing. It waits.

FinchTrade inverts this entirely. Under a post-trade settlement model with margin-based trading limits, clients post partial collateral (typically 30% of their trading limit) rather than the full notional amount. Trades execute against the agreed limit, settle automatically in approximately 30 minutes, and the limit resets. Capital stays in the client’s custody throughout. For a company running €10 million in monthly volume, the difference between 100% pre-funding and 15% collateral is the difference between €10 million locked and €1.5 million posted. That is a treasury management argument, not just a product feature.

“When we were building FinchTrade, we kept hearing the same thing from PSPs and EMIs: the liquidity was available, but the capital requirements made it operationally unworkable. So, post-trade settlement was not a product decision we made to be competitive. In fact, it was the only model that made sense for the clients we were actually trying to serve.” — Nicola Boldrini, growth lead at FinchTrade

Settlement Speed Is the Product

Thirty minutes is not an arbitrary benchmark. For the clients FinchTrade serves, settlement speed is the product itself.

A PSP accepting crypto on behalf of merchants needs fast conversion to fiat, or the merchant absorbs exchange rate risk on every transaction. A European EMI routing funds to Africa needs settlement to clear before downstream banking correspondents close. For both, slow settlement compounds across time zones into reconciliation overhead and cash-flow uncertainty that is difficult to manage at scale. Traditional OTC desks typically run T+1 with manual confirmation workflows. A consistent 30-minute cycle running around the clock removes the problem at source.

The Cross-Border Case: Africa, LATAM, and the UAE

Alongside the core OTC desk, FinchTrade has been developing cross-border payment corridor infrastructure aimed at the routes where SWIFT is weakest. The design targets Europe-to-Africa flows in Nigerian naira, Ghanaian cedi, and Kenyan shilling; Europe-to-LATAM corridors in Mexican peso, Brazilian real, Chilean peso, and Argentine peso; and Europe-to-UAE flows in dirham.

The model is straightforward. Where SWIFT’s correspondent banking runs T+3 to T+7, with fees compounding at each intermediary hop and AML exposure multiplying across a chain of counterparties, FinchTrade’s approach is built to replace that chain with a single counterparty: funds converted at institutional FX rates using stablecoins as the settlement medium, then delivered in local currency via domestic rails, with per-transaction reporting that includes FX rates, on-chain hashes, and bank references. The architecture is designed to settle on a T+0 or T+1 basis rather than the multi-day cycles correspondent banking imposes.

For businesses running regular B2B payments between European infrastructure and African or Latin American markets, the intended advantages are fewer intermediaries, faster settlement, transparent pricing, and a single audit trail. The cross-border product is structured under a Canadian FINTRAC registration, giving it its own compliance anchor for corridors that connect jurisdictions with very different regulatory maturity.

The Swiss VASP Advantage

Regulatory jurisdiction is not a formality for institutional clients. It is frequently the deciding factor in whether a relationship is commercially viable at all.

FinchTrade holds Swiss VASP registration and VQF membership, and is certified under ISO/IEC 27001 for information security management and ISO/IEC 27701 for privacy information management. ISO 27001 certification is a near-universal requirement for B2B technology vendors across financial services. Its presence signals that FinchTrade has implemented the controls that institutional compliance teams need to approve a new third-party relationship. The Swiss positioning also provides geographic optionality, sitting outside MiCAR and FCA perimeters, for clients in the Middle East, Asia-Pacific, Africa, and other non-restricted jurisdictions who need regulated infrastructure without the complexity of EU or UK authorisation.

Integration, Onboarding, and the Case Studies

For clients with engineering resources, FinchTrade offers a full API integration with WebSocket support for real-time lifecycle events, a sandbox testing environment, and documented endpoints covering onboarding, deposits, trading, and withdrawals. Time to production runs one to two weeks. For mid-sized OTC desks that prefer manual workflows, a managed service option sets up in approximately one day. Onboarding through automated KYC/KYB runs in one to five days, with human review in parallel.

The published case studies validate the architecture under real conditions. INXY, a crypto payment processor, grew monthly volume by approximately 18% after integrating FinchTrade as its primary liquidity provider, with deep liquidity pools reducing slippage and enabling non-standard requests that automated systems typically cannot handle. A third-party European OTC desk reported 45% faster execution on large trades, with over 80% of its crypto-to-fiat volume now running through FinchTrade on tighter spreads and higher fill rates.

FinchTrade at a Glance

|

Feature |

Detail |

|

Licence |

Swiss VQF VASP + ISO/IEC 27001 & 27701 |

|

Client type |

B2B only: PSPs, EMIs, OTC desks, exchanges |

|

Max single trade |

€10M |

|

Average settlement |

~30 minutes |

|

Onboarding timeline |

1-5 days |

|

Supported assets |

USDT, USDC, EURC, BTC, ETH, XRP, ADA, LTC, DOGE |

|

Supported networks |

Ethereum, Polygon, Solana, Tron |

|

Fiat currencies |

EUR, USD, GBP, CHF, AED |

|

Cross-border corridors |

Europe to Africa (NGN, GHS, KES), LATAM (MXN, BRL, CLP, ARS), UAE (AED) |

|

Pre-funding model |

Post-trade settlement, 10-20% partial collateral |

|

Banking partners |

BCB Group, ClearJunction, Nexpay, FV Bank, Fiat Republic |

|

Custody partner |

Fireblocks |

|

Support |

24/7 via Telegram and email |

|

Total volume (2025-2026) |

$1B+ |

FAQ

What is FinchTrade?

FinchTrade is a Swiss-licensed institutional OTC desk and crypto-fiat settlement provider serving B2B clients: payment service providers, electronic money institutions, crypto exchanges, and OTC desks. There is no retail product and no native token.

Is FinchTrade regulated?

FinchTrade operates under Swiss VASP licensing through the VQF self-regulatory organisation, holds ISO/IEC 27001 and ISO/IEC 27701 certifications, and operates its cross-border payments product under a Canadian FINTRAC registration. The platform is not MiCAR compliant and is not FCA regulated. Services are not offered to retail clients residing in, or corporate clients registered or established in, the UK, US, or EU.

Does FinchTrade require 100% pre-funding?

No. Clients maintain a trading limit and post partial collateral (typically 10-20% of that limit) rather than locking the full notional amount. Capital stays in the client’s custody and the trading limit resets automatically after each settlement cycle.

FinchTrade’s services are available to institutional and professional clients only and are not available to retail clients or corporate clients registered in the United Kingdom, United States, European Union, or other restricted jurisdictions. This article is for informational purposes only and does not constitute financial or investment advice.