Ondo Perps Review 2027: Can Tokenized Equity Collateral Transform 24/7 Markets?

Our flagship Ondo Perps review examines stock and commodity perpetuals, tokenized collateral, fees, leverage, SGX security, weekend trading, risks and the best alternatives.

Research Verified: 17 July 2026

Editorial Note: This 2027 edition is based on platform information verified in July 2026. Ondo Perps remains in Public Beta, so live specifications should be rechecked before publication or trading.

Executive Summary

Ondo Perps is building a derivatives exchange around a powerful premise: tokenized securities should not remain passive assets while traders post separate stablecoin collateral elsewhere.

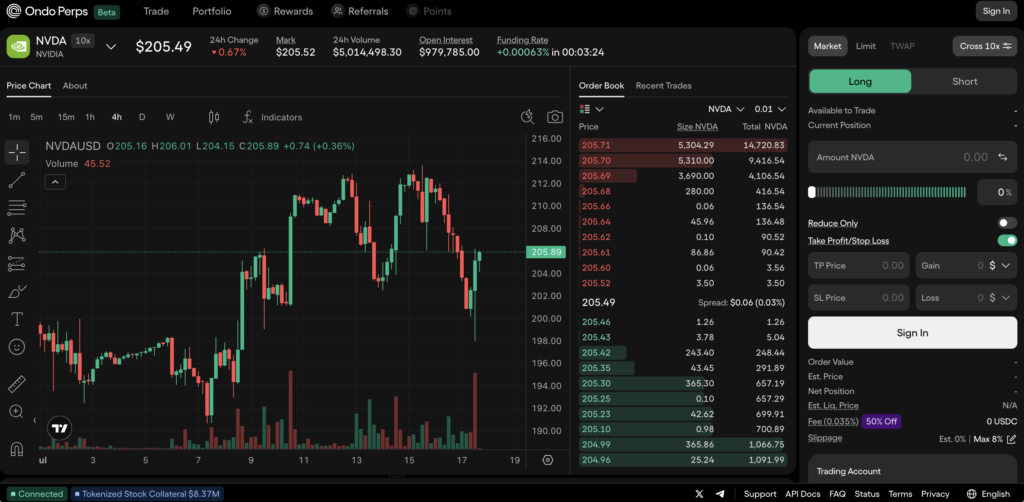

The platform allows eligible users to trade 24/7 perpetual futures linked to U.S. equities, indices, commodities and ETFs. More importantly, approved participants can use selected Ondo tokenized securities as margin, potentially placing a tokenized hedge asset and its related perpetual exposure inside the same capital system.

Execution takes place through an offchain order book running inside Intel SGX secure enclaves. Deposits and withdrawals remain onchain, while a distributed attestor network is intended to verify the deployed exchange software and prevent one operator from unilaterally controlling key material.

This design gives Ondo Perps CEX-like performance without following the architecture of either a standard centralised exchange or a fully onchain DEX.

Flagship verdict: Ondo Perps is one of the most strategically significant RWA derivatives experiments of 2026. Its technology and collateral model could improve capital efficiency for equity-perpetual markets. Its limitations are equally significant: cross margin is mandatory, tokenized collateral remains restricted, internal balances are tracked offchain, and users depend on SGX, attestors and omnibus hot-wallet infrastructure.

Referral code: P9N3ST

Ondo Perps at a Glance

Category | Ondo Perps |

Core product | Perpetual futures linked to real-world assets |

Market categories | Equities, indices, commodities and an ETF |

Current documented markets | 24 |

Maximum leverage | Up to 20x |

Margin mode | Cross margin only |

Standard collateral | USDC |

Limited-access collateral | SPYON and QQQON |

SPYON and QQQON haircut | 10% |

Maker fee | 0.015% |

Taker fee | 0.035% |

Position cap during Public Beta | $500,000 per market, per account |

Execution model | Offchain central limit order book |

Trusted execution | Intel SGX secure enclaves |

Verification model | Independent attestor quorum |

Deposit and withdrawal network | Ethereum |

Internal account balances | Tracked offchain |

Collateral storage | Omnibus operational wallet |

Order types | Market, limit, TP/SL, reduce-only, post-only and TWAP |

API infrastructure | REST and WebSocket |

Current development stage | Public Beta |

Tokenized collateral stage | Limited-access Pre-Alpha |

Restricted users | Includes U.S. and Panama residents plus other prohibited jurisdictions |

Decentralised News referral code | P9N3ST |

The current market, collateral, fee and beta-stage specifications above come from official Ondo Perps documentation reviewed on 17 July 2026.

Why Ondo Perps Matters

RWA perpetual exchanges face a structural capital problem.

A market maker may post USDC on a perpetual exchange while simultaneously holding shares, futures or cash at a traditional brokerage to hedge its exposure.

Both pools support one economic position, but the capital remains fragmented.

Ondo Perps attempts to place tokenized securities and related perpetual exposure in the same margin environment.

A participant making markets in an equity perpetual could theoretically hold the tokenized equity as collateral and hedge through the perpetual without maintaining an entirely separate stablecoin pool for the same exposure.

That does not guarantee deep liquidity. Market makers still need incentives, operational confidence, reliable redemption, robust data and risk controls. It does, however, address a genuine inefficiency in existing RWA derivatives infrastructure.

Architecture: Neither a Conventional CEX Nor a Fully Onchain DEX

Component | Function | Key Dependency |

Exchange engine | Order book, matching, accounts, positions and liquidations | Enclave software and operational availability |

Intel SGX enclave | Isolates exchange logic and encrypted order flow | Hardware integrity and correct implementation |

Attestor network | Verifies the running binary and distributes key material | Independent quorum integrity |

Chain engine | Monitors deposits and initiates withdrawals | Blockchain and wallet infrastructure |

Per-account deposit address | Identifies incoming user transfers | Correct address provisioning |

Omnibus hot wallet | Holds deposited collateral operationally | Key security and withdrawal controls |

Offchain account ledger | Tracks individual balances and positions | Accurate exchange-engine accounting |

Ethereum | Current deposit and withdrawal network | Network availability and confirmation times |

Ondo Perps describes itself as an offchain matching engine with onchain settlement. The exchange engine does not settle each trade directly on Ethereum. Instead, it updates balances and positions inside the attested environment, while deposits and withdrawals create externally visible blockchain transactions.

The Custody Question

The platform uses the phrase “onchain custody,” but the technical documentation also says deposits are swept into a main hot wallet and that individual balances are tracked offchain.

This distinction matters.

Users do not retain direct control of deposited collateral in the same way they retain control of assets sitting untouched in a personal wallet.

The platform’s security promise rests on:

- Attested exchange software

- Distributed key shares

- Quorum-controlled upgrades

- Public deposit and withdrawal records

- Withdrawal validation

- Operational wallet controls

That is a sophisticated model, but it is not identical to non-custodial smart-contract trading where users can independently verify every account balance and position onchain.

The Current Market Universe

Category | Markets | Maximum Leverage |

Equity | Apple | 20x |

Equity | AMD, Amazon, Coinbase, Circle, Alphabet, Robinhood, Intel, Meta, Microsoft, MicroStrategy, Netflix, Nvidia, Oracle, Palantir, SpaceX and Tesla | 10x |

Equity | Micron Technology | 5x on the current markets page |

Index | S&P 500 and Nasdaq 100 | 20x |

Commodity | Gold, silver and WTI crude oil | 20x |

ETF | Roundhill Memory ETF | 10x |

The live market page should take priority where another documentation page differs. At the time of review, Micron was shown as 5x on the market list but grouped with 10x equities on the leverage page.

What a Perpetual Position Does Not Provide

Perpetual Exposure | Direct Share Ownership |

Price exposure through a derivative | Legal ownership of the security |

Can go long or short | Usually requires borrowing or derivatives to short |

Funding may be paid or received | No perpetual funding mechanism |

Can use leverage | Brokerage margin rules apply separately |

No expiry while margin remains | Shares do not expire |

Corporate actions reflected through pricing | Corporate actions attach to the owned security |

Liquidation is possible | Fully paid shares are not normally liquidated for price decline alone |

Ondo Perps positions are derivatives. They should not be marketed as equivalent to purchasing the underlying securities.

Collateral: Where the Strategy Becomes Different

Collateral | Availability | Current Haircut | Margin Value of $10,000 |

USDC | All eligible accounts | 0% | Approximately $10,000 |

SPYON | Approved accounts | 10% | Approximately $9,000 |

QQQON | Approved accounts | 10% | Approximately $9,000 |

Deposited tokenized assets are priced using the corresponding exchange mark price. Haircuts are intended to account for price volatility, weekend gaps and conversion costs.

Tokenized collateral remained a limited-access Pre-Alpha feature when this article was researched. This means Ondo Perps’ most important strategic feature was not yet fully available to every public user.

Why the Haircut Matters

A trader may see a tokenized asset valued at $10,000 but receive only $9,000 of margin credit.

If the token declines, both its market value and available margin can fall.

A trader using SPYON as collateral while holding another leveraged position is exposed to:

- The value of SPYON

- The perpetual position

- Funding

- Cross-margin interactions

- Weekend pricing

- Liquidation thresholds

- Potential collateral-policy changes

Tokenized equity collateral creates capital efficiency, not free leverage.

Cross Margin and Account-Wide Liquidation Risk

Feature | Ondo Perps |

Cross margin | Supported and mandatory |

Isolated margin | Not supported |

Collateral pool | Shared across all positions |

Gains offset losses | Yes, at account level |

One position can affect others | Yes |

Liquidation assessment | Total account health |

Cross margin can be efficient for hedged portfolios.

A long technology-stock perpetual and a short Nasdaq position can offset part of each other’s economic risk. Available margin does not need to be assigned manually to each position.

The same architecture can amplify account-wide damage. A sharp loss in one large position can consume the collateral protecting every other trade.

Margin Requirements

Maximum Leverage | Initial Margin at Maximum Leverage | Maintenance Margin |

20x | 5% | 2.5% |

10x | 10% | 5% |

5x | Approximately 20% | Check live market configuration |

A 100% margin ratio triggers liquidation under the current documentation.

The platform’s Public Beta position cap is $500,000 per market and account, despite a separate page describing a $1 million margin bracket. The lower beta-stage cap remains the relevant practical limit.

Ondo Perps Fee Schedule

Fee Type | Current Rate |

Maker | 0.015% |

Taker | 0.035% |

Direct Fee by Executed Notional

Trade Size | Maker Fee | Taker Fee |

$1,000 | $0.15 | $0.35 |

$10,000 | $1.50 | $3.50 |

$100,000 | $15.00 | $35.00 |

$500,000 | $75.00 | $175.00 |

A $100,000 taker entry and taker exit would produce approximately $70 in direct trading fees before funding, spread and slippage.

Effective Trading Cost

Cost | When It Arises |

Maker or taker fee | Every executed order |

Spread | Entering and exiting through the order book |

Slippage | Order size exceeds available depth |

Funding | Position remains open through funding intervals |

Collateral haircut | Tokenized collateral receives less than full margin credit |

Liquidation cost | Account falls below maintenance requirements |

Weekend liquidity cost | Underlying markets are closed and order-book depth changes |

Funding: A Documentation Issue Traders Should Not Ignore

The official markets page lists eight funding intervals per day.

The key trading-concepts page says funding occurs hourly.

These descriptions cannot both be correct under a standard daily schedule.

Official Page | Stated Frequency |

Markets page | Eight intervals per day |

Key trading concepts | Hourly |

Practical response | Confirm the live countdown before trading |

The discrepancy is important because funding frequency affects holding costs, arbitrage calculations and projected liquidation risk.

The platform also states that equity-perpetual funding receives a 0.5x dampening multiplier, reducing the approximate baseline annualised rate from 11% to 5.5%. That baseline is not a guaranteed cost or return. Actual funding depends on market premium and positioning.

How Weekend Trading Changes the Risk Model

Traditional equity markets close. Ondo Perps does not.

Session | Primary Price Input |

Normal market hours | External pricing feeds |

Weekend or closed session | Internal order-book-derived oracle |

External reopening | Return to external pricing |

Liquidation reference | Multi-component mark price |

During normal hours, Ondo Perps uses pricing from external data providers including Pyth, Stork and other institutional sources.

During closed sessions, an internal oracle begins from the final external price and moves according to order-book pressure.

When external pricing resumes, the oracle returns to the external value.

Discovery Bounds

Maximum Market Leverage | Approximate Weekend Range Around External Close |

20x | Plus or minus 5% |

10x | Plus or minus 10% |

5x | Plus or minus 20% |

The formula is based on one divided by maximum leverage.

Orders that would execute outside the permitted range are rejected. The restriction is lifted when external pricing resumes.

The Weekend Paradox

A bounded price can reduce extreme internal manipulation, but it does not remove economic risk.

A material news event could imply a move larger than the allowed range. The perpetual may remain constrained during the weekend, then confront a large adjustment when external markets reopen.

This makes maximum leverage particularly dangerous over weekends and holidays.

Order Types and Execution Controls

Order Type | Main Use | Important Limitation |

Market | Immediate execution | Slippage |

Limit | Price-controlled entry | Fill not guaranteed |

Post-only | Seek maker status | Rejected if immediately marketable |

Reduce-only | Prevent position increase | Requires an existing exposure to reduce |

Take profit | Exit after favourable movement | Executes as a market order |

Stop loss | Exit after adverse movement | Can partially execute or fail |

TWAP | Split larger orders | Continues unless separately cancelled |

Ondo Perps supports market, limit, TP/SL and TWAP orders alongside reduce-only and post-only controls.

TP/SL Execution Risk

TP/SL orders trigger from the mark price and execute against the live order book as market orders.

Where liquidity is inadequate, only part of the position may close. The remaining stop is cancelled rather than queued for another attempt.

Stop-limit orders were not available when reviewed.

TWAP Parameters

Parameter | Current Setting |

Minimum duration | 5 minutes |

Maximum documented interface duration | 7 days |

Default interval | 30 seconds |

Other intervals | 1 minute, 5 minutes, 15 minutes and 1 hour |

Slippage guard | Maximum 3 basis points from initial mid-price |

Active TWAP limit | 20 per account |

Margin | Reserved upfront |

TWAP orders can reduce the visible impact of large trades, but they introduce workflow risk. A TP/SL order can close the existing position while the TWAP continues submitting new child orders.

API and Professional Trading Infrastructure

Capability | Availability |

REST API | Documented |

WebSocket API | Documented |

Public market channels | Available |

Private account channels | Available with authentication |

Batched orders | Supported |

TWAP API | Supported |

Stop-order API | Supported |

Funding history | Supported |

Position monitoring | Supported |

API IP whitelist | Supported |

New key creation in Public Beta | Disabled by default |

API keys can be permissioned, and up to 16 IPv4 addresses can be added to an IP whitelist. An empty whitelist permits requests from any IP, making explicit configuration important.

Existing keys remain active during Public Beta, while new key creation requires platform approval.

Security Assessment

Positive Security Characteristics

Control | Intended Benefit |

SGX enclave | Isolates exchange logic and order flow |

Reproducible builds | Lets attestors compare deployed and published binaries |

Independent attestors | Reduces unilateral operator control |

Distributed key shares | Prevents one party from reconstructing key material |

Quorum-gated upgrades | Limits silent software modification |

Onchain deposits and withdrawals | Makes external asset movement visible |

Mark-price median | Reduces reliance on one price input |

Mark-price clamping | Slows extreme one-cycle changes |

Position caps | Restricts beta-stage exposure |

Cantina bug bounty | Incentivises vulnerability reporting |

The platform advertises regular third-party audits, although no specific report with clear scope and findings was located in the documentation reviewed. Ondo Perps also maintains a Cantina bounty with an advertised maximum reward of $1.5 million in USDC.

Unresolved Security Questions

- Which exact exchange-engine version received each third-party audit?

- Are complete reports publicly accessible?

- How geographically and organisationally independent are the attestors?

- What happens if SGX vulnerabilities affect the deployed hardware?

- How much collateral can reside in the operational hot wallet?

- What emergency withdrawal procedures exist during an enclave or attestor outage?

- How are conflicting attestor states resolved?

- What insurance capital is available relative to open interest?

- What recovery process applies if offchain account data becomes unavailable?

These questions do not prove a weakness. They identify information sophisticated traders should seek before maintaining large balances.

Ondo Perps Risk Matrix

Risk | Potential Impact | Practical Mitigation |

Cross-margin contagion | One position affects the whole account | Reduce leverage and separate capital |

Liquidation | Forced closure and loss of collateral | Maintain a large margin buffer |

Weekend gap | Abrupt repricing at external reopening | Reduce weekend exposure |

Funding | Holding costs erode returns | Check live funding before entry |

Oracle error | Incorrect margin or liquidation reference | Avoid maximum leverage |

SGX vulnerability | Exchange integrity or wallet logic affected | Limit account balances |

Attestor failure | Verification or key operations disrupted | Monitor platform status |

Hot-wallet compromise | Operational collateral at risk | Keep long-term assets elsewhere |

Offchain ledger failure | Account or position access disrupted | Export records and limit exposure |

API compromise | Unauthorised trades | Use minimum permissions and IP whitelists |

Tokenized collateral decline | Lower account margin | Maintain excess USDC |

Public Beta changes | Rules or access can shift | Recheck parameters frequently |

Regulatory restrictions | Account access may be limited | Confirm jurisdictional eligibility |

Ondo Perps Pros and Cons

Advantages | Disadvantages |

Purpose-built RWA perpetual venue | Public Beta |

Stock, index, commodity and ETF markets | Limited market count |

Trading available 24/7 | Weekend pricing complexity |

Leverage of up to 20x | High liquidation risk |

Tokenized securities can become collateral | Feature remains limited-access |

Low published maker and taker fees | Funding and spread still matter |

Institutional-style order book | Internal accounting is offchain |

Encrypted order execution | Reliance on Intel SGX |

Distributed attestor network | Attestor-network risk |

Public deposits and withdrawals | Omnibus hot-wallet exposure |

TWAP and API support | New API keys restricted during beta |

No per-trade gas cost | Cross margin only |

Email and wallet onboarding | No isolated margin |

Order-book discovery outside market hours | Reopening gaps remain possible |

Best Ondo Perps Alternatives for 2027

No platform simultaneously dominates RWA coverage, crypto liquidity, self-custody, execution speed and regulatory access.

The alternatives below use materially different architectures. Affiliate relationships do not affect the need for independent research.

On-Chain and Hybrid Alternatives

Platform | Best Compared For | Affiliate Access |

Ostium | On-chain macro and real-world markets | |

gTrade | Forex, commodities, indices and synthetic markets | |

Aster | Crypto and real-world perpetual markets | |

Paradex | Order-book derivatives and advanced trading | |

Lighter | Performance-oriented verifiable order-book trading | |

edgeX | Professional decentralised perpetual execution | |

Aevo | Crypto perpetuals, options and pre-launch markets | |

GMX | Pool-based EVM perpetual trading | |

ApeX Omni | Multi-chain deposits and API-driven perpetual trading | |

MYX | Alternative perpetual-liquidity architecture |

Centralised Futures Alternatives

These platforms primarily compete for crypto-derivatives activity rather than Ondo Perps’ tokenized-equity collateral niche.

Platform | Best Compared For | Affiliate Access |

Bybit | Broad derivatives, bots and active trading | |

MEXC | Extensive altcoin-futures selection | |

Bitget | Derivatives, bots and copy trading | |

BingX | Social and copy-trading tools | |

BloFin | Futures-oriented professional interface | |

Bitunix | Streamlined perpetual-futures trading | |

KCEX | Fee-sensitive crypto-futures trading | |

Deribit | Specialist crypto options and derivatives |

Which Platform Fits Each Trader?

Priority | Platform to Research |

Tokenized equity collateral | Ondo Perps |

Stock and index perpetuals | Ondo Perps, Ostium, gTrade or Aster |

Gold and commodity perpetuals | Ondo Perps, Ostium or gTrade |

Fully crypto-focused derivatives | Bybit, MEXC, Bitget or BloFin |

Crypto options | Deribit or Aevo |

Pool-based EVM execution | GMX |

Verifiable order-book infrastructure | Lighter |

Advanced decentralised order book | Paradex or edgeX |

Copy trading | Bitget or BingX |

API-driven professional trading | Ondo Perps, ApeX Omni, Bybit or Deribit |

Isolated margin | Research alternatives, since Ondo Perps is cross-margin only |

Direct stock ownership | A regulated securities broker, not a perpetual exchange |

How to Use Ondo Perps More Carefully

- Confirm that your jurisdiction is eligible.

- Use the official Decentralised News referral link.

- Begin with USDC rather than complex tokenized collateral.

- Keep leverage well below the maximum.

- Treat all positions as one cross-margined portfolio.

- Check the live funding countdown.

- Review weekend discovery bounds.

- Reduce exposure before major earnings or market closures.

- Use reduce-only controls.

- Do not assume a stop order will fill the entire position.

- Cancel an active TWAP after another order closes the position.

- Use API IP whitelisting.

- Maintain independent trade and deposit records.

- Complete a small withdrawal test.

- Keep long-term investments outside the exchange account.

Final Ondo Perps Review Verdict

Ondo Perps is not merely another perpetual exchange adding a few synthetic stocks to a crypto interface.

Its central innovation is collateral architecture.

Tokenized securities can potentially become active trading capital, allowing market makers and hedgers to use an equity-linked asset and its perpetual market inside the same system.

If this model attracts serious market makers, it could produce more efficient RWA derivatives than stablecoin-only platforms.

The execution architecture is also ambitious. Intel SGX, encrypted order processing and distributed attestation attempt to provide centralised-exchange performance without granting one operator complete control over matching logic or wallet keys.

The trade-off is that users must trust a more complex stack.

Assets are swept into an operational wallet. Account balances are maintained offchain. Secure hardware, software reproducibility, attestors and withdrawal infrastructure all have to work as intended.

The platform’s current maturity also matters. Ondo Perps remains in Public Beta, tokenized collateral is restricted, API access is controlled and some documentation pages disagree on material parameters.

Our conclusion is therefore balanced.

Ondo Perps is one of the most important RWA derivatives platforms to watch, but it remains an advanced and evolving product rather than a low-risk retail trading account.

Experienced traders may find genuine value in its market access, fees, execution and collateral model. Beginners should first understand cross margin, funding, weekend gaps and the difference between perpetual exposure and owning a security.

Referral code: P9N3ST

Frequently Asked Questions

Is Ondo Perps legitimate?

Ondo Perps is a live Public Beta platform with documented markets, account infrastructure, APIs and security architecture. Being operational does not make it risk-free or suitable for every user.

Is Ondo Perps decentralised?

It uses a distributed attestor network and secure enclaves, but matching and account balances are offchain. Deposits and withdrawals occur onchain.

Does Decentralised News have an Ondo Perps affiliate link?

Yes. Use the Decentralised News Ondo Perps link.

The referral code is P9N3ST.

Does the referral code guarantee a bonus?

No guaranteed benefit should be assumed unless the live platform explicitly displays one.

Can I trade stocks on Ondo Perps?

You can trade perpetual futures linked to selected stocks. You are not purchasing the underlying shares.

Can I receive dividends?

Perpetual holders do not receive dividends in the same way as direct shareholders. Corporate actions are reflected through the platform’s pricing mechanisms.

What is the maximum leverage?

Selected markets offer up to 20x. Others currently offer 10x or 5x.

Does Ondo Perps have isolated margin?

No. All positions currently use cross margin.

What are the fees?

The current maker fee is 0.015%, and the taker fee is 0.035%.

Is trading available 24/7?

Yes. The exchange remains open when traditional markets are closed, using an internal pricing system during extended sessions.

What happens when the stock market is closed?

External feeds stop genuine price discovery, and Ondo Perps switches to an internal oracle based on order-book activity and defined discovery bounds.

What collateral does Ondo Perps accept?

USDC is broadly available. Approved accounts can apply to use SPYON and QQQON with a 10% haircut.

Is tokenized stock collateral publicly available?

It remained a limited-access Pre-Alpha feature when this review was researched.

What blockchain does Ondo Perps use?

Ethereum currently handles deposits and withdrawals.

Where are trades executed?

Matching, margin and liquidations occur offchain inside Intel SGX secure enclaves.

Does Ondo Perps have an API?

Yes. REST and WebSocket APIs are documented, although new API-key creation is restricted during Public Beta.

Is there an Ondo Perps audit?

The platform advertises third-party audits, but this review did not locate a specific publicly linked report with a complete scope and findings.

Does Ondo Perps have a bug bounty?

Yes. A Cantina programme advertises rewards of up to $1.5 million in USDC.

Is Ondo Perps available in the United States?

No. U.S. persons and residents are not eligible under the current documentation.

What are the best alternatives?

Leading alternatives to research include Ostium, gTrade, Aster, Paradex, Lighter, edgeX, Aevo, GMX, ApeX Omni, MYX, Bybit, MEXC, Bitget, BingX, BloFin, Bitunix, KCEX and Deribit.

Affiliate Disclosure

The Ondo Perps referral link and certain alternative-platform links are affiliate links. Decentralised News may receive compensation or platform rewards when eligible users register or transact through them.

Affiliate relationships do not influence our assessment of fees, security, architecture, risks or platform suitability.

Educational Disclaimer

This article is provided for educational and informational purposes only. It is not financial, investment, legal, trading or tax advice.

Perpetual futures and leveraged products can result in rapid and total loss of capital. Tokenized collateral can decline in value while supporting other leveraged positions. Secure enclaves, attestors, APIs, oracles, blockchains, matching engines and operational wallets can fail or be compromised.

Platform specifications, markets, funding schedules and legal availability can change. Verify all live information before depositing or trading. Never trade with money you cannot afford to lose. For adults aged 18 and over.